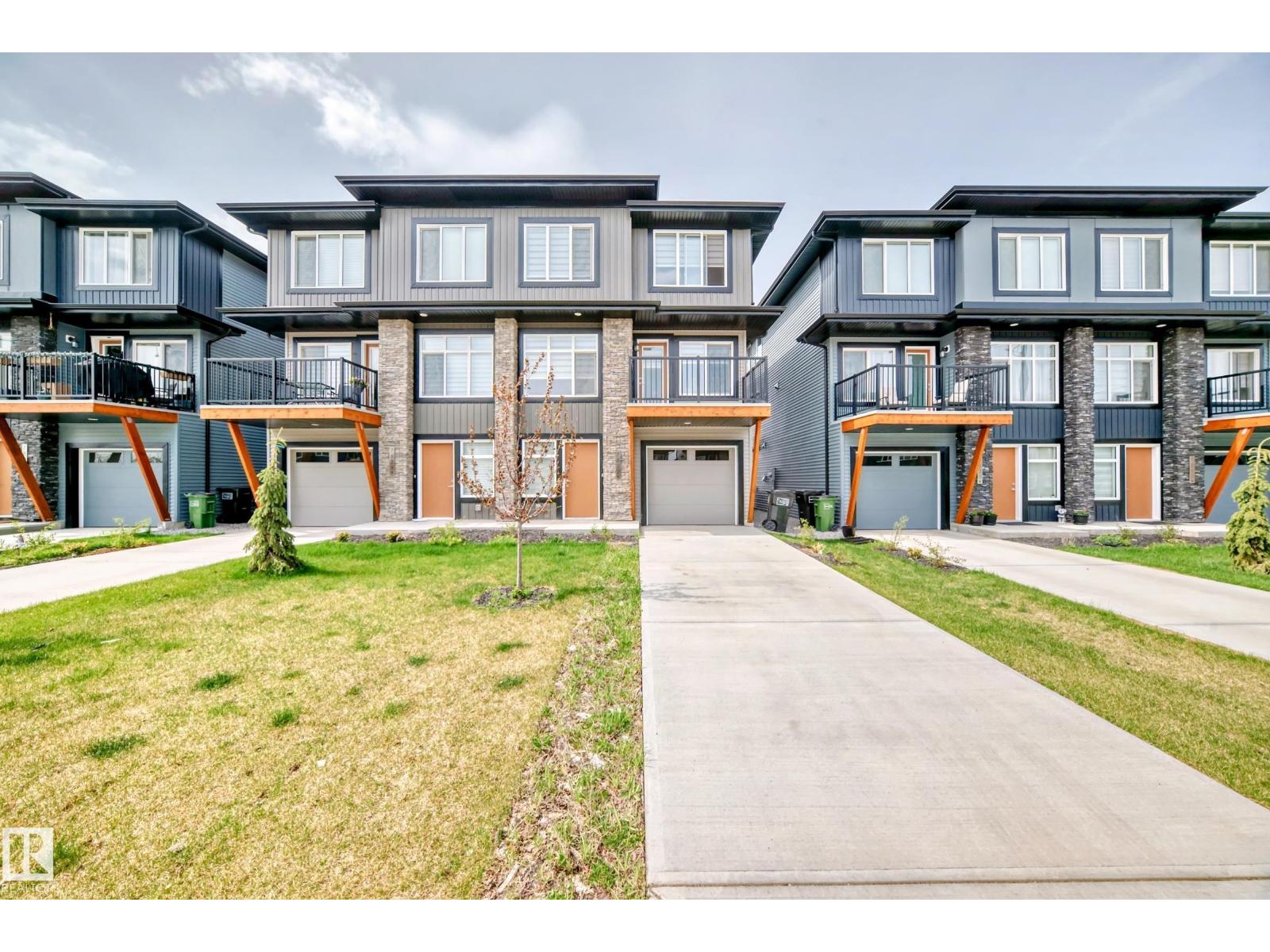

A modern Keswick townhome with no condo fees and a path to ownership.

End unit, three storeys, attached garage, private balcony. One of SW Edmonton's fastest-growing communities. Get in now at today's price.

- No Condo Fees

- 3 bedrooms + flex

- 3 bathrooms

- 1,606 sq ft

- End unit

- Attached garage + 2 stalls

- Private balcony

- 2023 build

The short version

Per month, total

Covers your rent and Monthly Option Consideration ($750/mo), which contributes toward your future down payment.

To start

Your Initial Option Consideration. Credited in full against the purchase price when you exercise the Option.

Months to buy

Your future purchase price is pre-agreed at signing. Three years to get mortgage-ready — with a plan and support to get there.

Inside the home

About the home

- StyleEnd unit townhome

- Year built2023

- Square feet1,606

- Storeys3

- Bedrooms3 + flex space

- Bathrooms3 full

- Condo feesNone

- GarageSingle attached

- Driveway stalls2

- NeighbourhoodKeswick, SW Edmonton

What stands out

- End unit — extra windows, more natural light, more privacy

- No condo fees, ever

- Private balcony — great for BBQs and summer evenings

- Open concept main floor with upgraded stainless steel appliances

- Primary bedroom with walk-in closet and ensuite

- Flex space for a home office, playroom, or guest room

- Single attached garage plus two driveway stalls

- Minutes to shopping, schools, Terwillegar trails, and golf courses

- 2023 build — modern finishings throughout, no deferred maintenance

Why rent-to-own this home

Keswick is one of southwest Edmonton's most in-demand new communities. Great schools, trails, golf, and easy access to the Anthony Henday — the kind of neighbourhood where values hold. This home was built in 2023, which means no aging systems, no surprise repairs, and modern finishings you'd actually want.

The end unit position matters more than people realize. You get extra windows on the side, more natural light, and a sense of space that middle units just can't offer. The flex space and three full bathrooms mean a household of four — or five — actually fits comfortably.

And there are no condo fees. Your monthly number is your monthly number.

Move in now. Own it on your terms.

What it costs

Here's the full picture — nothing hidden. Your monthly payment, your future down payment, and what the numbers look like on the other side when you own it.

Utilities are paid by you. All figures are based on current list price and program terms. Your exact payment is confirmed at pre-qualification.

Your future down payment

- Current list price

- $414,800

- Initial Option Consideration

- $20,000

- Term

- 36 months

- Condo fees

- None

- Utilities

- Paid by you

Your future purchase price is pre-agreed at signing based on your term and projected appreciation. Full breakdown shared at pre-qualification.

Who this fits

Our program is built for motivated buyers who need a clear path, not a miracle.

Credit rebuild

You had a consumer proposal, a rough patch, or a recent job change, and the bank said no. You need time and a plan to get there.

Self-employed

You run a business and your tax return doesn't reflect what you actually earn. Banks struggle with that. We don't.

New to Alberta

You relocated and need time to build Canadian credit, savings, or both before a traditional mortgage will work for you.

Not sure if you fit? Start the pre-qualification anyway. If it's not a match, we'll tell you straight.

How it works

Pre-qualify online

A quick two-minute form tells us if the numbers fit. No credit pull at this stage.

Meet our broker

You sit down with Danelle Cole, our mortgage expert, to map out a plan to qualify by the end of your term.

Move in

Pay your option consideration, sign the paperwork, and get your keys. The home is yours to live in.

Buy the home

Follow the plan. At the end of your term, you exercise your option and take title on the place.

Questions buyers ask

Are there really no condo fees?

Correct — none. This is a freehold townhome, not a condominium. There is no condo corporation and no monthly fee on top of your payment. Your $3,525/month covers rent and your Monthly Option Consideration. Utilities are separate and paid by you.

What is rent-to-own, actually?

You sign two agreements: a Residential Tenancy Agreement (the lease) and an Option to Purchase Agreement (your exclusive right to buy at a pre-agreed future price). You pay rent plus a Monthly Option Consideration. At the end of your term, you exercise the Option and buy the home. Your total Option Fee — the $20,000 upfront plus all monthly contributions — is credited against the purchase price at closing.

What happens if I don't exercise the Option at the end of my term?

Per the Option to Purchase Agreement, 90% of your total Option Fee is retained by the Grantor and 10% is returned to you within 30 days, less any amounts you owe. We and our mortgage broker work with you throughout the term to keep you on track — so this outcome is avoidable with the right plan in place from day one.

Is my $20,000 refundable?

Your $20,000 is the Initial Option Consideration — the fee that grants you the exclusive right to purchase this home at the pre-agreed future price. If you exercise the Option and close, the full $20,000 is credited against the purchase price. If you don't exercise, the 90/10 retention rule above applies. Full terms are in the Option to Purchase Agreement you'll review before signing.

Who handles repairs?

You pay for a home inspection before move-in and sign off on the home's condition. From that point, all repairs and maintenance are your responsibility — day-to-day upkeep and major items alike. A 2023 build means you're starting with everything new, which significantly reduces the risk of surprise costs in the early years.

Can I buy before the 36 months are up?

Our program requires a minimum of 12 months before you can exercise the Option. If you qualify for a mortgage earlier, talk to us and we'll coordinate the timing. If early exercise means breaking our underlying mortgage, those penalty costs pass through to you.

Can I see the home first?

Yes. Once you pre-qualify and the numbers check out, we book a showing. We don't run showings for people who haven't pre-qualified — it wastes everyone's time, including yours.

Ready to see if this home is yours?

Pre-qualification takes about two minutes. You'll know right away if the numbers work.

Start pre-qualification